Uncovering the Ultimate Exchange: A Comparison of Vertex Competitors

The rapidly evolving world of DeFi is transforming the way we think about crypto trading and ownership. The search for the ideal crypto exchange that aligns with the true principles of decentralization, while simultaneously ensuring efficiency and versatility, has often led to a dead-end. We're excited to introduce Vertex Protocol: a cutting-edge, vertically integrated decentralized exchange (DEX) set to disrupt this status quo.

Vertex is an absolute game-changer in the DeFi space. It's an exchange that doesn't compromise on capital efficiency, user experience, and self-custody, a true first in crypto. Let’s see how the Goliaths of crypto trading– dYdX, Binance, GMX– stack up against this new DEX on Arbitrum.

How to Evaluate an Exchange

The utility of an exchange can be evaluated on several metrics.

- Fees

- Exchange infrastructure and Latency

- Protection against Frontrunning & MEV

- Cross-Margin and Capital Efficiency

Fees and Latency

Perhaps the most important metric is transaction fees. Lower fees enhance profitability, especially for high-volume traders. Some exchanges will also differentiate between maker and taker fees. Makers add liquidity to the exchange, so they are sometimes compensated for their service through lower fees (or even rebates). The second metric is latency, or the speed at which orders are processed. One can think of latencies as the time it takes for a placed market order to be filled, or the time it takes for a trader to receive confirmation that his limit order was added to the orderbook. Lower latencies can offer a competitive edge in volatile markets, and are imperative for many automated traders.

Exchange Infrastructure

The next set of metrics are the exchange infrastructure used to provide liquidity and price discovery. Some crypto exchanges use on-chain Automated Market Makers (AMM), which facilitate passive liquidity provision and support long-tail assets. These are typically DEXs. AMMs are simple to use, both for liquidity providers and for directional traders trading against the liquidity pool. A central limit order book (CLOB) may also be used to facilitate price discovery by aggregating and displaying limit orders across a spectrum of prices and quantities. Most DEXs do not use CLOB due to the difficulty of building a gas-efficient CLOB on-chain. We usually see centralized exchanges (CEX) using a CLOB. Additionally, an API or SDK is required to make the exchange convenient for automated traders such as HFTs and institutional market makers. They use the exchange infrastructure to provide liquidity and well-aligned prices via arbitrage with other venues.

Protection Against Frontrunning & MEV

An exchange's protections against frontrunning and Maximum Extractable Value (MEV) must also be considered. MEV unfairly benefits malicious validators at a cost to honest traders. One weakness of the on-chain AMM model is the potential for a high amount of flows to be frontrunning and toxic. This hurts passive liquidity providers. A CLOB enables first-in-first-out (FIFO) sequencing, which mitigates frontrunning. The bottom line is that both methods have certain tradeoffs which should be clarified to the end user.

Cross-Margin and Capital Efficiency

Finally, cross-margined accounts allow traders to automatically share collateral across their open positions and have their unrealized PNL count toward collateral requirements. Cross-margin accounts enable unparalleled capital efficiency, and indeed very few exchanges offer it. Even when they do, the account is often restricted to a certain kind of tradable instrument. For instance, cross-margining may occur for spot products only, so the PNL from open perps positions might not count toward the collateral of a leveraged spot position.

The best form of cross-margin is therefore more aptly named “universal cross-margin.” It is universal because it necessitates the integration of spot, derivatives, and money markets into a single stack, and risk-managed by a coherent set of enforceable standards. This is the only way the unrealized PNLs of spot and derivative positions alike can be automatically applied to the margin requirements of each other. Universal cross-margin has a very similar concept in traditional finance (TradFi), called portfolio margin.

The Baseline of Comparison

The astute reader might have noticed that many of these criteria are generally applicable to the stock, options, and futures exchanges which facilitate TradFi securities trading. TradFi exchanges tend to have institutional market makers providing deep liquidity via automated strategies on CLOBs. Strict risk management rules, such as those outlined in SPAN or Regulation T, are also enforced. Indeed, the ease by which centralized entities can provide such superior user experience is precisely the reason CEXs tend to dominate crypto trading today.

Now that we have a baseline of what to look for in an exchange, let's see how incumbent crypto exchanges stack up. You’ll also see why Vertex Protocol changes the game completely.

Binance

Binance is easily the biggest cryptocurrency exchange today. Founded in 2017 by Changpeng Zhao (aka “CZ”), the platform quickly gained prominence due to its comprehensive suite of features, robust security measures, and a vast array of supported cryptocurrencies. Binance is a CEX which offers spot and perpetuals trading.

~ Fees

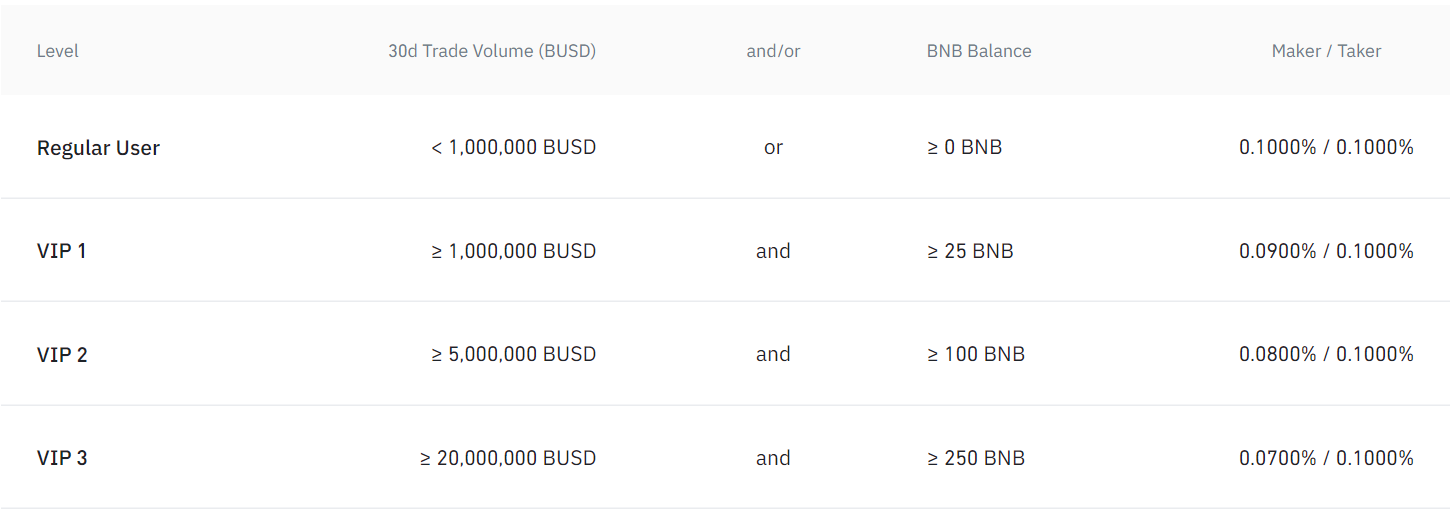

Binance’s fees are 0.10% of the trade size for spot assets. It makes no distinction between maker and taker flow for regular users with less than $1 million in 30-day trading volume. As volume increases, maker fees go down but takers still pay 0.10%.

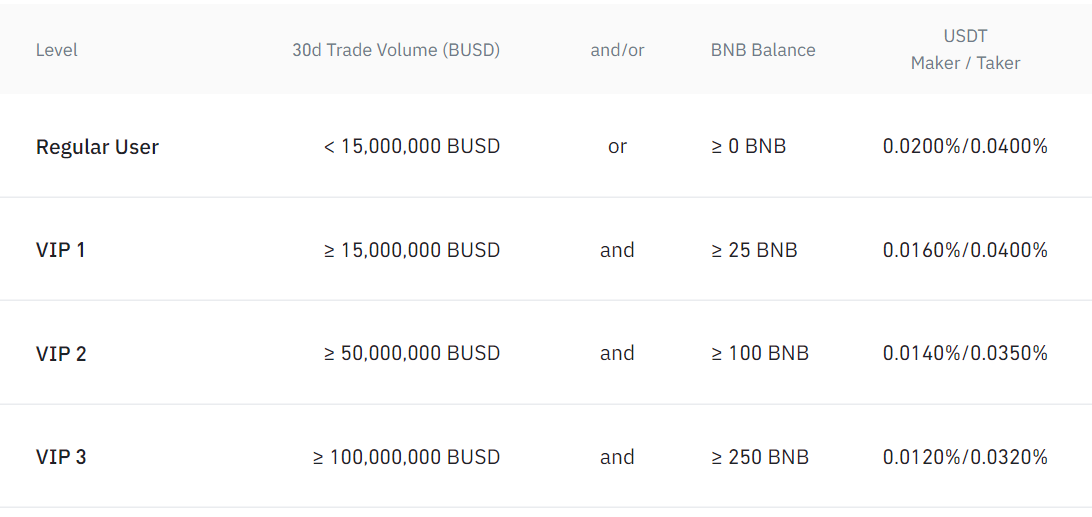

Binance’s perpetuals and futures fees are lower. Regular users start off at 0.02% for makers and 0.04% for takers. It’s evident that these fees are lower than those on nearly all DEXs. From this alone we can see the strong economic incentive to trade on Binance. Of all the exchanges covered in this article, only Vertex offers lower fees than Binance on all fronts.

~ Exchange Infrastructure

Binance has an extremely low 5 millisecond latency. This is the lowest among the exchanges we’ll cover today. Binance uses a CLOB to match orders and does not support AMMs, so passive liquidity provision is impossible. It also rules out the possibility for easily listing long-tail assets which tend to have thin CLOB liquidity but can still be supported by an AMM.

For many years traders have used the Binance API to execute algorithmic trading strategies. The API helps institutional traders connect to Binance so they can supply liquidity to the orderbook or enter and close out of fast directional trades. This creates a better user experience for retail traders as well.

~ Protection Against Frontrunning & MEV

Binance maintains a largely off-chain state, and is not subject to MEV. Orders are served on a FIFO basis and the likelihood of frontrunning is identical to that of TradFi exchanges. Through the Binance API, advanced traders may back out any evidence of frontrunning, which protects them from such malicious activities.

~ Cross-Margin Accounts

Binance has cross-margin capabilities, though this is not the default feature. Users may create up to 10 sub-accounts and dictate what kind of trading is enabled within each account. These are effectively isolated margin accounts. Traders may also create a single cross-margin account where all trading pairs are available. However, it’s important to note that this cross-margin account is not universal. The account may be cross-margin for perpetuals and futures only, or for leveraged spot only, but never for both. Binance has cross-margin, but it is a step short from meeting the gold standard of capital efficient trading.

Of course, Binance’s generally superior user experience and product suite is largely achieved via its centralization. It seems the tradeoff for convenience is to give up user self-custody and transparency. Based on Binance’s success, this has been a tradeoff which people have been willing to make.

dYdX

Founded by Antonio Juliano in 2017, dYdX has emerged as one of the leading DEXs in the DeFi space. dYdX offers an off-chain CLOB for perpetuals trading, which is uncommon in the DEX landscape. While the initial version of dYdX was built on the base layer of Ethereum, later versions have been created on faster Layer 2’s. dYdX is currently building v4, and it’s intended to be fully decentralized as a sovereign application blockchain built with the Cosmos SDK.

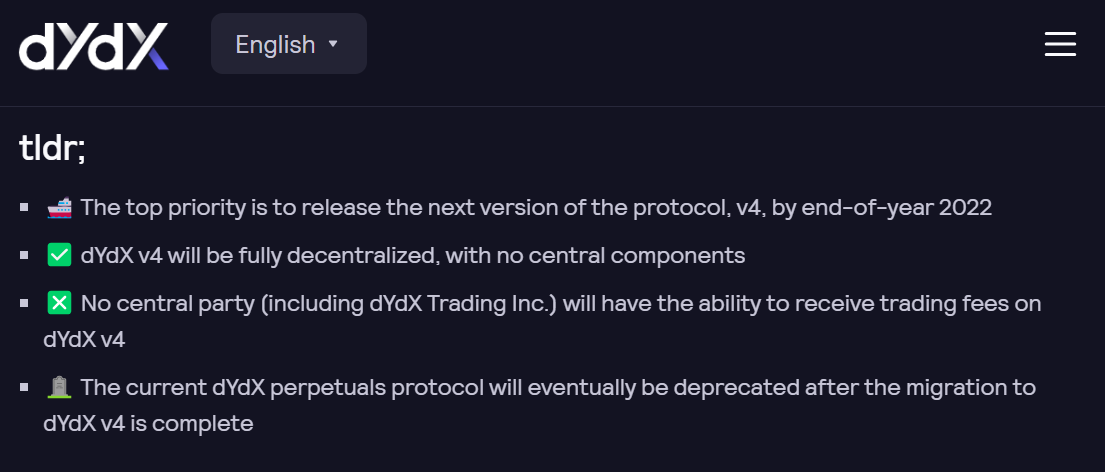

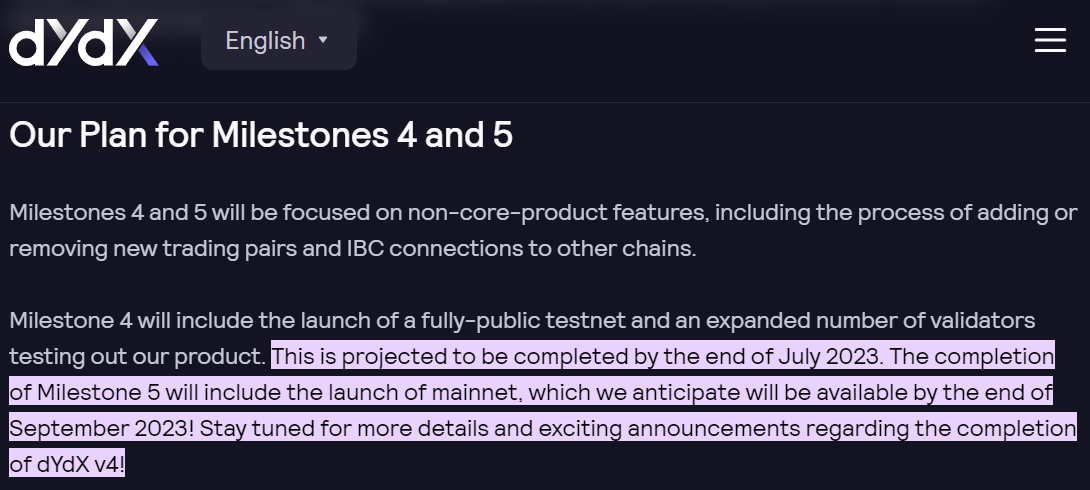

Creating a fully decentralized and efficient trading venue is admittedly challenging. The launch date has been postponed a few times. The above picture shows a summary of v4, and lists the end of 2022 as the planned release date. However, as of Q2 2023, v4 is yet to be released and the new projected launch is at the end of September 2023.

As a quick aside, there are some issues with an MEV-resistant, on-chain CLOB. DEXs such as Injective and Sei– both on-chain, MEV-resistant CLOBs built with the Cosmos SDK– use frequent batch auctions (FBA) to create MEV-resistance. FBA causes all transactions to settle at the same price at discrete times, usually standardized to block time. This indeed disables frontrunning. The problem is it also effectively removes the bid-offer spread, a market maker’s primary source of revenue. Thus, traditional market makers will not trade on such venues, hurting liquidity in the long run. Based on dYdX’s blog posts, v4 will make use of “in-memory” orderbooks maintained by the app-chain’s validators. Clearly, this will not be MEV-resistant as validators will have the ability and incentive to sort transactions into value-extractive arrangements.

But what about the latest current version, dYdX v3, built on StarkWare? A quick glance at the v3 API documentation reveals that there is no spot trading on v3. Spot trading is still available through the previous versions, but these versions are not connected to v3 by any meaningful economic mechanism.

Sadly, the team does not prioritize adding spot trading to v3 nor to the upcoming v4. This is an issue for the capital efficient execution of common strategies like basis trades or funding rate capture. Universal cross-margin involves integrated spot and perp markets at a minimum, so dYdX v3 is automatically not such a venue.

~ Fees

Perhaps the biggest benefit of dYdX is its low fees. For example, the first $100,000 in volume across a 30-day period is free. After that, makers pay 0.02% and takers pay 0.05%. When 30-day volume begins to exceed $1 million, both maker and taker fees start to go down. These are very cheap fees in the DEX space, many times lower than DEX competitors like GMX, which we’ll look at next.

~ Exchange Infrastructure

As mentioned, dYdX has an API which can be used by automated traders to execute their strategies. v3 makes use of an off-chain CLOB to process trades. Taking order matching off-chain and settling them on-chain can seriously reduce exchange latency. Because it’s not straightforward to find a latency number stated by dYdX, we reached out through their customer support channel to gain some clarity. It turns out that the oracle price feed’s latency is roughly 1000 milliseconds. However, this will be a bit different from the latency for processing an order.

Based on the estimates of others we’ve talked to, including a market maker, dYdX’s latency for processing orders seems to sit squarely below the 1 second mark. For instance, one contact from Dexterity said it was around 500 milliseconds. A market maker told us it was around 50 milliseconds. Altogether, we can conclude that dYdX’s latency sits comfortably below 1000 milliseconds.

Also, it goes without saying that dYdX has some great customer support, as we were able to get a clear response almost immediately through the chat on their website. Customer support couldn’t shed light on v4’s expected latency, but we can expect that it will also be around this current estimate. The fastest Cosmos chain is probably Sei, which has a block time around 500 milliseconds. Cosmos’ Tendermint consensus usually has block times of a few seconds. Therefore, 1000 milliseconds as an upper-bound is an educated guess for v4’s latency.

~ Protection Against Frontrunning & MEV

The second benefit of v3’s off-chain CLOB is that it is purely FIFO and therefore MEV resistant. That is very helpful to traders who want to use a DEX but are, understandably, turned off by the possibility of being frontrun while using on-chain infrastructure.

Overall, dYdX is a premium DEX. We are excited to see what v4 has to offer!

GMX

GMX is a popular DEX operating on the Arbitrum and Avalanche networks. GMX stands out in the crowded DEX landscape by offering both spot and perpetual trading, facilitated by a unique liquidity pool model designed for capital efficiency and zero price-impact trades.

~ Fees

Fees are relatively high on GMX. Spot fees (called “swap fees”) can range from 0.20% to 0.80%. Perpetual fees are 0.10% of the trade size. The capital from GMX’s liquidity providers, which is collectively called GLP, serves as the counterparty for GMX traders. Therefore, there's a difference between takers and makers on GMX versus those on other platforms. Technically speaking, the “makers” are the liquidity providers of GLP, and they earn 70% of the fees paid by the traders, who are technically the “takers.” However, makers and takers are normally defined by limit orders versus market orders. Limit orders “make” liquidity by adding quotes to the CLOB while market orders “take” liquidity by filling those quotes and removing them from the CLOB. In the case of GMX, GLP neither uses limit orders nor market orders– only GMX traders use them. And, there is no distinction between the trading fees paid by limit orders versus those paid by market orders. Thus, there is no practical difference between maker and taker fees on GMX. This is a stark difference from the other exchanges we’ve seen.

That said, 0.20% to 0.80% is rather high for spot fees. Uniswap commonly charges 0.30% for spot fees. The 0.10% perp fee is also rather large when compared to the exchanges covered in this article.

~ Exchange Infrastructure

The main appeal of GMX seems to be the zero-price impact trades and the ability to wield up to 50x leverage. On top of this, GLP is an elegant model which generates substantial real yield because GMX traders as a whole (GLP’s counterparty) tend to lose. This yield contributes to the appeal of the GMX ecosystem.

There are, however, a few weaknesses to the GMX design. To begin, the GLP model is not scalable. When GMX traders take a perp position, they are effectively borrowing assets from the liquidity pool. In fact, GMX is arguably closer to a leveraged spot protocol than a perp protocol. The problem is that traders are basically constrained by the TVL of GLP and fees can get very big if a certain trade is in high demand and incurs higher borrow fees. Moreover, any tradable product on GMX is tightly entangled with the other assets in GLP. To add a new asset, the composition of GLP must change, and this will directly impact every liquidity provider. Thus, although GMX is an on-chain AMM, it is not an AMM which supports long-tail assets. These GLP shortfalls are clearly the tradeoffs for zero-price impact.

Furthermore, GMX has no orderbook, no API or SDK. Because it doesn’t source liquidity from traditional market makers the way dYdX and Binance does, there isn’t really a need for these things. Traders who would like to use automated strategies on GMX must put in undue effort to build out their own infrastructure.

And there’s more bad news. By being fully on-chain, GMX’s latency is dependent on the block time of its underlying chain. On both Arbitrum and Avalanche, it can take several seconds for an order to be recognized by the protocol. This is a pretty high latency, and it can make traders quite vulnerable during times of high volatility. GMX is the slowest exchange covered here.

~ Protection Against Frontrunning & MEV

GMX has no defense against MEV, a feature that is guaranteed to hurt traders over time. This just piles over on top of consistently losing, high fees, and unscalable markets.

~ Cross-Margin Accounts

Finally, GMX has no cross-margined accounts. Despite having the mechanisms of a spot liquidity pool, and what resembles a money market, GMX offers no way for positions to withstand premature liquidation from an isolated margin shortfall. Even though positions might have positive unrealized PNL, this “excess capital” is never automatically counted towards the the margin requirements of other positions in need of margin.

GMX is truly a retail-only dApp. Its design strikes the delicate balance of simple and versatile as an avenue for highly leveraged, adrenaline-seeker trades. The casino is expensive, and the house tends to win. Serious institutional traders are probably staying away.

Vertex Protocol

The final exchange we’ll cover here is Vertex Protocol. Vertex is a Hybrid Orderbook-AMM DEX built on Arbitrum which facilitates universal cross-margined accounts, spot, perps, money markets, and lightning fast trade execution. The bottom line is that Vertex objectively meets all outlined qualities for evaluating an exchange. Let’s dive in.

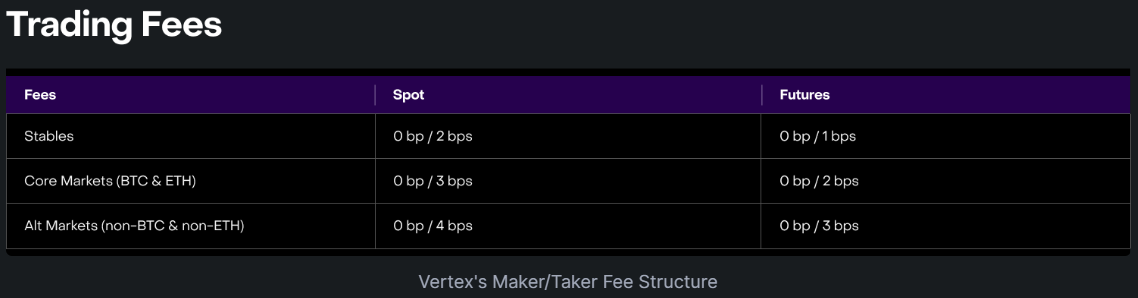

~ Fees

Vertex has the cheapest fees of all exchanges mentioned here. Makers always trade for free on Vertex regardless of product. Taker fees for the “core” BTC and ETH markets are 0.03% and 0.02% for spot and perps, respectively. This means Vertex’s perp fees for the two core markets are automatically as cheap as dYdX’s “VIP level” tier (which only applies to 30-day volumes over $200 million!).

In the other markets, taker fees are just a single basis point higher for spot and perps. Vertex’s fees are much cheaper than the others (assuming one goes over $100,000 a month on dYdX) and is guaranteed to attract capital from advanced market participants over time.

~ Exchange Infrastructure

Vertex has a high-end latency of 15 milliseconds thanks to its state-of-the-art off-chain sequencer which hosts Vertex’s CLOB. Most of the time, Vertex latencies are in the high single digit. Automated traders can connect directly with the sequencer via the Vertex API or SDK. Vertex offers both options, allowing traders to pick whatever suits them best.

The name Vertex is short for “vertically integrated exchange.” One of its unique value propositions is that spot, perp, and money markets are rolled into a single decentralized platform. This alone is something truly new to DeFi as no other DEX has managed to efficiently combine all three markets. DeFi has traditionally fallen short on versatility because useful features have been spread out across multiple platforms. Go to Aave to borrow or lend, to Uniswap to trade spot assets, and to dYdX for perpetuals. Now, people can do all three on Vertex.

~ Universal Cross-Margin Accounts

As we noted, vertical integration across spot, derivatives, and money markets is a requirement for universal cross-margin. We are pleased to announce that Vertex is the first crypto exchange to our knowledge which offers this unparalleled level of capital efficiency. On Vertex, unrealized PNL from perpetual trades can automatically be used as collateral for leveraged spot positions, and vice versa. Unlike Binance, there is no distinction between spot and perps when it comes to utilizing the overall value of a position. On top of universal cross-margin accounts, Vertex will also enable an unlimited number of sub accounts usable for isolated margin. Binance users may only create up to 10 sub accounts. Best of all, Vertex achieves all of this whilst the user enjoys full transparency and self-custody.

~ Protection Against MEV… But Wait There’s More!

Another notable feature about Vertex’s design is its Hybrid Orderbook-AMM. This ensures Vertex users can enjoy the best of both worlds. The off-chain orderbook offers lightning-fast sub-second trade executions with FIFO treatment and total protection from MEV. The on-chain AMM offers a permissionless liquidity backstop where traders can force their trades to occur, albeit at higher latencies. This is affectionately called “Slo-Mo Mode,” and it may be used during rare instances of a sequencer malfunction. The Vertex AMM democratizes liquidity provision, and its unique role in the vertically integrated exchange is also supplemented by allowing liquidity providers to deposit their LP tokens as margin collateral for perp or leveraged spot trades. Such synergistic use cases for LPs are only possible on Vertex. The AMM also supports Vertex’s ability to list long-tail assets, allowing it to become a liquidity launchpad for prospective projects in the DeFi and Web3 space.

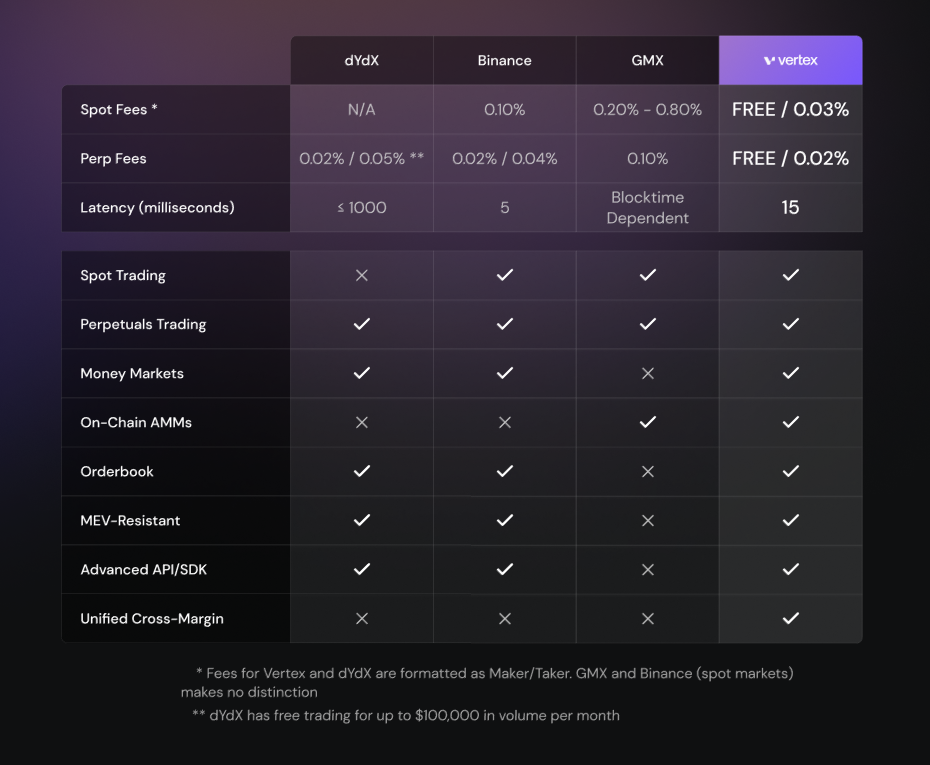

Unlike GMX, Vertex was designed to be highly scalable. Each new market is simply another entry to the smart contracts which handle on-chain risk management on a modular basis. Over the next month, Vertex will roll out over a dozen new markets, which will collectively capture the vast majority of underlying assets used for crypto trading today. Very soon, most crypto trading can be done on the deep liquidity, low fees, and high throughput of Vertex. And that goes for retail and institutional traders alike. Below is the exchange comparison table which summarizes what we covered today.

Conclusion

The purpose of this article was to introduce user-centric metrics for evaluating exchanges and then to evaluate incumbent crypto exchanges along these metrics. Readers may have noticed that topics like decentralization were glossed over to favor deeper discussion of features which actually have an impact on daily user experience. Vertex was designed ultimately with the User in mind. How can users retain the fundamentals of self custody and transparency while having superior user experience? From the carefully crafted frontend to the intricacies required for on-chain universal cross-margin, Vertex was built to bring convenience to DeFi so people no longer have to choose between versatility and security.

It’s clear that no other exchange, DEX or CEX, offers the unique features of Vertex Protocol. The thing is, our fellow Volumooors, this is only the beginning.

Stay tuned.😉